Warren Buffett's Favorite Type of Business

Disclaimer: This page contains some affiliate links that might just lead you to the promised land of awesomeness (or at least some cool products). I personally use all of the products promoted, and recommend them because they are companies I have found to be helpful and trustworthy. I may receive commissions for purchases made through links in this post.

They say reading Warren Buffett’s annual shareholder letters is like getting a free MBA in investing. As someone who’s passionate about investing—and who didn’t even finish his bachelor’s degree—I figured it wouldn’t hurt to read through them myself.

So far, I’ve read and taken notes on each letter up through the early 1990s (Investment Club members get full access to all my notes), and in every letter, there are at least a few memorable takeaways that have helped me learn something new.

The other day, I stumbled upon a real gem going through the 1991 letter. In it, Warren makes an important distinction between two types of businesses: the first, which he calls an “economic franchise,” and the second, which is just a regular business.

According to Buffett, an economic franchise is what you should be looking for. This type of business has special qualities that give it an edge, and to qualify as an economic franchise, it has to meet three criteria:

First, people have to want—or better yet, need—its products. This is true for any successful business, but with an economic franchise, demand has to be steady and long-lasting.

I think Procter & Gamble (PG) exemplifies this pretty well. People will always need essentials like toothpaste, diapers, and toilet paper, and it’s nearly impossible to imagine a world where they don’t. This kind of consistent demand makes Proctor & Gamble hard to replace and, at least in my opinion, ensures it will stay relevant well into the future.

The second thing that defines an economic franchise is that customers don’t see other companies’ products as a good substitute. In the mind of the customer, there is no replacement.

Although some will definitely disagree, I think Starbucks (SBUX) checks this box. Even though there are countless other places to get your morning cup of joe (and get it cheaper), many people still choose to make Starbucks a part of their daily routine.

They could go to Dutch Bros. (BROS) or some other purveyor, but they don’t, because only Starbucks can deliver the experience they want. Plus, it’s habitual—and habits are hard to break.

To be fair, the reverse can be true as well. Some people prefer Dutch Bros. over Starbucks for similar reasons. Either way, the point is that customers consider these experiences to be irreplaceable in their routines.

With that, the third and final ingredient for an economic franchise is that the business needs the freedom to adjust its prices without being hindered by regulation. Having this freedom allows the company to raise prices and grow profits, hopefully without losing customers in the process.

Intuit (INTU) is a great example of a company that can pull this off. People rely on Intuit’s software for essential tasks like bookkeeping and filing taxes, and switching to another platform would be a hassle. As a result, if Intuit raises its prices, the great majority of its customers are likely to stick around.

According to Buffett, when a company has all of these qualities, it’s more than just a regular business. There’s something special about it that investors would be wise to investigate.

On the other hand, regular businesses don’t have all of these advantages. For a regular business to perform well over time, it usually has to do one of two things.

One option is to be the lowest-cost operator. This means being more efficient than competitors so it can charge lower prices and still make a profit.

I think Walmart (WMT) is a shining example of this. It competes by offering the lowest prices possible, which it achieves by keeping its costs low and operating at razor-thin margins.

While that certainly stands to benefit customers, the downside for lowest-cost operators like Walmart is that customer loyalty only goes as far as the low prices. If competitors could get in there and outprice Walmart, many customers would follow.

Alternatively, a regular business might also see exceptional profits during times of high demand and limited supply. This happens quite often with oil and gas companies.

Oil prices can skyrocket when demand is high, but supply is limited. This is when companies like ExxonMobil (XOM) or Chevron (CVX) can see a major boost in profits. But these high-demand periods are typically only temporary, as supply eventually catches up, bringing prices and profits back down to earth.

Overall, it’s clear to see why Buffett would prefer to invest in an economic franchise over a regular business. With their unique strengths and competitive advantages, franchises tend to make more stable, profitable, and resilient investments over a long period of time. Plus, who wants to be regular, anyway?

With all of that said, I’d love to hear from you: Which businesses would you consider to be economic franchises? Write to me here and let me know.

And click here if you want to learn about a great business that I’ve been loading up on in my portfolio.

Dividend Investing Democratized

Join thousands of savvy investors in the pursuit of early retirement. Get Retire With Ryne delivered straight to your inbox every week as you build your perpetually growing, cash-flowing dividend stock portfolio.

Blossom is a unique social platform created by investors, for investors. Unlike the usual social media platforms, Blossom is dedicated exclusively to discussions on finance and investing.

I've been actively posting on Blossom since November, and I absolutely love the community over there. With over 120,000 DIY investors, Blossom is buzzing with all sorts of different investment ideas. The coolest part is that you can see everyone's portfolios, which you can automatically link within the app!

Picture Twitter/X, but with an added portfolio tracking feature and less trolling – that's Blossom for you. Personally, I find it much more enjoyable than my experience on Twitter/X, and I think you will too.

Download Blossom today, and follow me (@ryne) to see my complete portfolio and stay updated on all my real-time investment moves.

IN MY PORTFOLIO 📈

Portfolio performance provided by Snowball Analytics

ICYMI 🎥

These 5 Dividend Stocks Made My Portfolio SKYROCKET

2024 has been one of the best years on record for my dividend portfolio! Since last November, my portfolio has exploded in value, a lot of which is thanks to these five stocks.

CAREFULLY CURATED 🔍

📺 7 AI Proof Stocks- The buzz around AI is that it's taking over the world, but these seven dividend growth stocks prove that there’s still room for businesses with staying power, pairing strong returns on capital with physical products or services that AI can’t easily replace.

🎧 The Story of Costco - The not-so-short story of Charlie Munger's favorite company, Costco. This 3-hour episode of the Acquired podcast is a deep-dive that leaves no stone unturned.

📚 Bad News For REITs - REITs have been on a wild roller coaster ride through the second half of 2024, and this article dives into the twists and turns that are driving this uncertainty.

SINCE YOU ASKED 💬

"Do you ever feel like you are limiting yourself by only investing in dividend stocks? Especially when you are missing out on amazing returns from companies like SOFI and PLTR recently?"

- Johnny | YouTube

This is a fantastic question, and one I get a lot.

To be honest, I don’t feel like I’m missing out at all. My portfolio is having one of its best years ever!

In fact, since I started posting videos on YouTube (October 15, 2020), my dividend portfolio has actually outperformed the S&P 500. Of course, that could change down the road, but so far, things are looking great.

Source: Charles Schwab | Portfolio performance since 10/15/2020

With that said, I think this question highlights a common myth about dividend stocks: the belief that buying them locks you into a life of subpar returns. People often think that dividend stocks = poor performance, but that’s just not true.

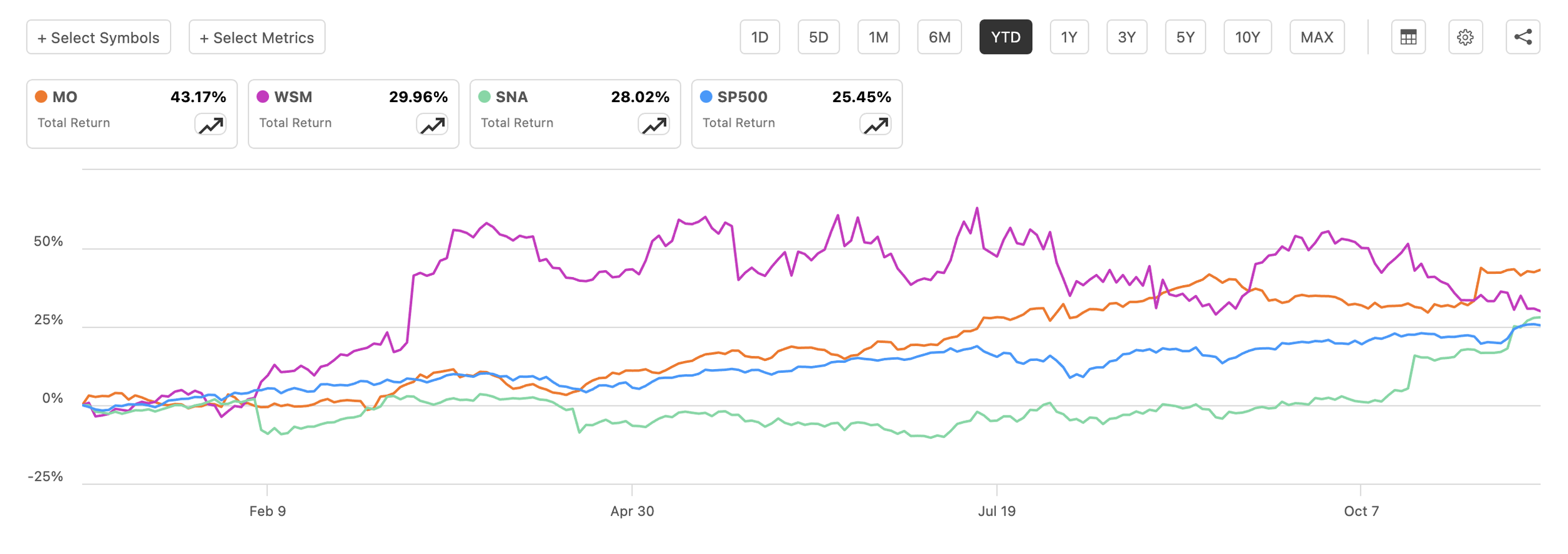

There are plenty of dividend-paying companies delivering strong results. For example, this year, while the S&P 500 is up around 25.5% on a total return basis, Altria Group (MO) has climbed 43.2%, Williams-Sonoma (WSM) is up 30%, and Snap-on (SNA) has gained 28%—and those are just examples from my portfolio.

Source: Seeking Alpha

But let’s be real: does year-to-date performance actually mean anything? At the end of the day, what is a year other than the time it takes the earth to go around the sun? Short-term performance doesn’t—and shouldn’t—carry much weight when it comes to ultimately determining the success of your investments.

Now, when it comes to companies like SOFI or PLTR, I’m perfectly fine not owning them.

I'd be willing to bet that, at this stage in the game, many of the people who invest in those companies are chasing the hype and riding the wave of positive momentum those companies are currently enjoying. That's not a strategy I particularly care to partake in.

If I'm correct (and I may not be), what we're seeing play out is a situation where the share prices of those companies are becoming increasingly detached from their intrinsic values. This will ultimately lead to a bubble.

The more hype builds, the higher the price will climb—until the momentum drives it to a critical point where it can no longer be sustained. There will inevitably be some straw that breaks the camel’s back, triggering an eventual correction that will bring the share price back down to earth.

When that happens, many of the people who bought into the hype will make their exits, which tells you that they never believed in the business itself. To me, that isn’t investing—it’s something else.

To close the book on this, I’m not worried about missing out on whatever the hot stock is at the moment. PLTR and SOFI may be having their moment today, but sooner or later, something new will come along to replace them—and the cycle will repeat.

I’m happy sticking to my strategy and investing in solid, proven businesses that deliver results over the long haul.

With that, as Russ would say, there's more than one way to get to financial heaven, and I sincerely hope that PLTR, SOFI, and all the other hype-driven stocks turn out to be substantial money-makers for those who own them.

Have a question? Ask me here to see it featured in an upcoming newsletter.

HOT TAKES 🔥

In last week's newsletter, I asked readers to tell me about the most recent milestones they hit in their portfolios. Here are some of the responses:

James said: The most recent milestone I hit was going over 700 shares of WMT and my portfolio hit over $87k in an all-time high. The road to 100k is closing quickly!

Lisa said: I just hit $50,000 in my dividend portfolio last week! This has been a big goal of mine since I started, and I’m thrilled to finally reach it!

Caleb said: I just doubled my dividend income from where I started this year. The next milestone I want to hit is $1,000 of annual dividend income and I think I can get there sometime in the next few months.

LAST WORD 👋

I recently had the opportunity to be a guest on Seeking Alpha's "Investing Experts" podcast to talk all things dividend stocks. Being an avid user and advocate of the platform since I started investing, this was a pretty surreal experience, and it was a lot of fun too!

I'd love for you to check out the episode and let me know your thoughts. You can listen to it here.